finance lease journal entries

WebThis video shows how the lessee would account for a lease classified as a finance lease under the new lease accounting rule. document.write('

WebThis video shows how the lessee would account for a lease classified as a finance lease under the new lease accounting rule. document.write(' For an operating lease as all cash outflows are classified as "operating" in the statement of cash flows. For each account, determine if it is increased or decreased. Lets walk through a lease accounting example. The entries for the first month of transition will be slightly different than subsequent months and for new leases. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The CPA Journal Everything is already on the balance sheet to begin with. Criteria 4: Is the present value of the sum of the lease payments substantially all of the fair value of the leased asset? If it's a new lease or you don't want to apply the practical expedient offered. The remeasurement journal entry is then: The closing balance of right of use asset value at 2021-10-15 is $24,550.34. If you would like greater detail on the concept of present valuing and the different options available, refer here. As a result, this lease is classified as a finance lease per the fourth test. Gross Profit Method Impact of overstating the gross profit %, 3 Reasons to use Universal CPA as a supplement for the CPA exam, net present value of future minimum lease payments. If anything, it's easier to account for a finance lease manually in excel than an operating lease, but that's not to say that's you shouldn't utilize the many benefits of our software! Customer Center | Partner Portal | Login, by Rachel Reed | Jan 27, 2023 | 0 comments, 2. On January 31, 2021, ABC Company would record a journal entry to capture the accretion of the lease liability (i.e., remeasure the present value of future payments), amortize the right-of-use asset, and record lease expense. In this examples modification, its the future lease payments that have been modified. Thus, under the new standard, a lease is a finance lease if any of the following conditions is met at inception: In addition, the new standard does not permit the lessee to exclude a guarantee of residual value from the lease payments by obtaining an insurance policy for the benefit of the lessor. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. As a result, in this example, the value of the right of use asset will be $116,375, the same amount as the lease liability. XYZ Ltd. charges a total of $1,500 in the lease transaction. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. Within the finance and banking industry, no one size fits all. This is the monthly Interest on the Lease Liability calculated as the Discount rate divided by 12* Prior Month's EOM Long Term & Short Term Liability (less BOM Payment). The lease term is 3 years while the remaining useful life of the forklift is 5 years. This has a flow-on impact on a company's cash flow statement. Financial Modeling & Valuation Analyst (FMVA), Commercial Banking & Credit Analyst (CBCA), Capital Markets & Securities Analyst (CMSA), Certified Business Intelligence & Data Analyst (BIDA), Financial Planning & Wealth Management (FPWM), Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. In some lease agreements, the payment is due at the end of the year, so the lease liability account balance would equal the equipment account balance in this initial entry. The rest of the revenue is demonstrated over the ensuing months of the lease term. Furthermore, most debt covenants calculations exclude operating leases as debt. Required fields are marked *, Please complete the equation below: * The interest expense for a operating lease is also classified as a lease expense, but the calculation follows the identical methodology as a finance lease. As of Jan. 1, 2022, the Financial Accounting Standards Board (FASB) lease accounting standard, Accounting Standards In a direct financing lease, the lessor acquires an asset and leases it to a customer/lessee to generate revenue from the resulting interest payments. Structured Query Language (known as SQL) is a programming language used to interact with a database. Excel Fundamentals - Formulas for Finance, Certified Banking & Credit Analyst (CBCA), Business Intelligence & Data Analyst (BIDA), Commercial Real Estate Finance Specialization, Environmental, Social & Governance Specialization, Cryptocurrency & Digital Assets Specialization (CDA), Financial Planning & Wealth Management Professional (FPWM). var plc459496 = window.plc459496 || 0; Therefore, this is a finance/capital lease because at least one of the finance lease criteria is met during the lease, and the risks/rewards of the asset have been fully transferred. As payments are made, the lease liability should ultimately unwind to $0. : These are the critical judgemental inputs when calculating the lease liability: When calculating the lease liability, the first step is to work out the known future payments at the start of the lease. Because the lessee who controls the asset is not the owner of the asset, the lessee may not exercise the same amount of care as if it were his/her own asset. Alamgir Table of Contents: What is Finance and Operating Lease? If the lessee obtained an insurance policy from a third-party guarantor to guarantee the residual value of the leased asset to the lessor at the end of the lease term, it could exclude the guaranteed amount from its minimum lease payments calculation so as to stay below the 90% investment recovery test threshold. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Straight line amortization of ROU Asset over the useful life/lease term. Cradle Inc. Because there has been a change to the lease liability value, and in this case, the value has increased, it results in a credit to the balance given its a liability. All rights reserved. The payment will be allocated between lease liability and interest expense and amortization expense will be recognized. Finance Lease Under the following circumstances,the lease transactions are called Finance lease 1. Toronto, ON M5C 1X6 The SEC staff presented the results of an empirical study which determined that approximately 63% of issuers reported offbalance sheet operating leases, with associated undiscounted future cash flows of nearly $1.25 trillion(Report and Recommendations Pursuant to Section 401(c) of the Sarbanes-Oxley Act of 2002 On Arrangements with Off-Balance Sheet Implications, Special Purpose Entities, and Transparency of Filings by Issuers,http://bit.ly/2tnZ3Eq).

For an operating lease as all cash outflows are classified as "operating" in the statement of cash flows. For each account, determine if it is increased or decreased. Lets walk through a lease accounting example. The entries for the first month of transition will be slightly different than subsequent months and for new leases. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The CPA Journal Everything is already on the balance sheet to begin with. Criteria 4: Is the present value of the sum of the lease payments substantially all of the fair value of the leased asset? If it's a new lease or you don't want to apply the practical expedient offered. The remeasurement journal entry is then: The closing balance of right of use asset value at 2021-10-15 is $24,550.34. If you would like greater detail on the concept of present valuing and the different options available, refer here. As a result, this lease is classified as a finance lease per the fourth test. Gross Profit Method Impact of overstating the gross profit %, 3 Reasons to use Universal CPA as a supplement for the CPA exam, net present value of future minimum lease payments. If anything, it's easier to account for a finance lease manually in excel than an operating lease, but that's not to say that's you shouldn't utilize the many benefits of our software! Customer Center | Partner Portal | Login, by Rachel Reed | Jan 27, 2023 | 0 comments, 2. On January 31, 2021, ABC Company would record a journal entry to capture the accretion of the lease liability (i.e., remeasure the present value of future payments), amortize the right-of-use asset, and record lease expense. In this examples modification, its the future lease payments that have been modified. Thus, under the new standard, a lease is a finance lease if any of the following conditions is met at inception: In addition, the new standard does not permit the lessee to exclude a guarantee of residual value from the lease payments by obtaining an insurance policy for the benefit of the lessor. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. As a result, in this example, the value of the right of use asset will be $116,375, the same amount as the lease liability. XYZ Ltd. charges a total of $1,500 in the lease transaction. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. Within the finance and banking industry, no one size fits all. This is the monthly Interest on the Lease Liability calculated as the Discount rate divided by 12* Prior Month's EOM Long Term & Short Term Liability (less BOM Payment). The lease term is 3 years while the remaining useful life of the forklift is 5 years. This has a flow-on impact on a company's cash flow statement. Financial Modeling & Valuation Analyst (FMVA), Commercial Banking & Credit Analyst (CBCA), Capital Markets & Securities Analyst (CMSA), Certified Business Intelligence & Data Analyst (BIDA), Financial Planning & Wealth Management (FPWM), Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. In some lease agreements, the payment is due at the end of the year, so the lease liability account balance would equal the equipment account balance in this initial entry. The rest of the revenue is demonstrated over the ensuing months of the lease term. Furthermore, most debt covenants calculations exclude operating leases as debt. Required fields are marked *, Please complete the equation below: * The interest expense for a operating lease is also classified as a lease expense, but the calculation follows the identical methodology as a finance lease. As of Jan. 1, 2022, the Financial Accounting Standards Board (FASB) lease accounting standard, Accounting Standards In a direct financing lease, the lessor acquires an asset and leases it to a customer/lessee to generate revenue from the resulting interest payments. Structured Query Language (known as SQL) is a programming language used to interact with a database. Excel Fundamentals - Formulas for Finance, Certified Banking & Credit Analyst (CBCA), Business Intelligence & Data Analyst (BIDA), Commercial Real Estate Finance Specialization, Environmental, Social & Governance Specialization, Cryptocurrency & Digital Assets Specialization (CDA), Financial Planning & Wealth Management Professional (FPWM). var plc459496 = window.plc459496 || 0; Therefore, this is a finance/capital lease because at least one of the finance lease criteria is met during the lease, and the risks/rewards of the asset have been fully transferred. As payments are made, the lease liability should ultimately unwind to $0. : These are the critical judgemental inputs when calculating the lease liability: When calculating the lease liability, the first step is to work out the known future payments at the start of the lease. Because the lessee who controls the asset is not the owner of the asset, the lessee may not exercise the same amount of care as if it were his/her own asset. Alamgir Table of Contents: What is Finance and Operating Lease? If the lessee obtained an insurance policy from a third-party guarantor to guarantee the residual value of the leased asset to the lessor at the end of the lease term, it could exclude the guaranteed amount from its minimum lease payments calculation so as to stay below the 90% investment recovery test threshold. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. Straight line amortization of ROU Asset over the useful life/lease term. Cradle Inc. Because there has been a change to the lease liability value, and in this case, the value has increased, it results in a credit to the balance given its a liability. All rights reserved. The payment will be allocated between lease liability and interest expense and amortization expense will be recognized. Finance Lease Under the following circumstances,the lease transactions are called Finance lease 1. Toronto, ON M5C 1X6 The SEC staff presented the results of an empirical study which determined that approximately 63% of issuers reported offbalance sheet operating leases, with associated undiscounted future cash flows of nearly $1.25 trillion(Report and Recommendations Pursuant to Section 401(c) of the Sarbanes-Oxley Act of 2002 On Arrangements with Off-Balance Sheet Implications, Special Purpose Entities, and Transparency of Filings by Issuers,http://bit.ly/2tnZ3Eq).  2022 Universal CPA Review.

2022 Universal CPA Review.  There are several inputs when determining the discount rate. c) Ensure the lase liability correctly unwinds to $0 with the updated formulas for each row.

There are several inputs when determining the discount rate. c) Ensure the lase liability correctly unwinds to $0 with the updated formulas for each row.  From this spreadsheet, you can derive the correct journals from now on. . The only exception is for leases with a term of 12 months or less. To calculate the straight-line amortization is the opening value of the right of use asset divided by the number of days of the useful life. WebAt the commencement of the lease, the lessor under IFRS 16 Lessor Accounting accounts for the finance lease by making the following journal entries: 2. May 16, 2022 What is the Accounting for a Sales-Type Lease? How to calculate cash to accrual adjustment for deferred revenue? It is worth noting, however, that under, This step-by-step guide covers the basics of lease accounting according to IFRS and, Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to. The lease liability account is reduced annually by an amount equivalent to the finance leases interest expense, and lastly, the equipment account is reduced by the difference between the lease expense and the lease liability change. We refer to those meeting only the third, fourth, or fifth criterion as weak-form finance leases. The new lease accounting standard recently became effective for private companies. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. Download our free present value calculator to perform the calculation. Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to identify finance leases. The Payments from 1st - 15th of first month of lease will be excluded from Liability (in PV calculation) but included in the ROU Asset. WebFinance lease and operating lease liabilities should be presented separately from each other and from other liabilities on the balance sheet or disclosed in the notes to the financial statements along with the balance sheet line items in which those liabilities are included. The purpose of this article is to introduce the main features of the new FASB standard and provide illustrations of how accounting and financial statement presentations for lessees will change. = var div = divs[divs.length-1]; The calculation of the lease liability follows identical principles. As a result the calculation will be $28,546.45 / 77 = $370.73. WebThe ownership is shifted to the lessee Lessee A Lessee, also called a Tenant, is an individual (or entity) who rents the land or property (generally immovable) from a lessor (property owner) under a legal lease agreement. Its important for your company to establish its own thresholds for these tests, document them in an internal accounting policy, and follow them consistently.

From this spreadsheet, you can derive the correct journals from now on. . The only exception is for leases with a term of 12 months or less. To calculate the straight-line amortization is the opening value of the right of use asset divided by the number of days of the useful life. WebAt the commencement of the lease, the lessor under IFRS 16 Lessor Accounting accounts for the finance lease by making the following journal entries: 2. May 16, 2022 What is the Accounting for a Sales-Type Lease? How to calculate cash to accrual adjustment for deferred revenue? It is worth noting, however, that under, This step-by-step guide covers the basics of lease accounting according to IFRS and, Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to. The lease liability account is reduced annually by an amount equivalent to the finance leases interest expense, and lastly, the equipment account is reduced by the difference between the lease expense and the lease liability change. We refer to those meeting only the third, fourth, or fifth criterion as weak-form finance leases. The new lease accounting standard recently became effective for private companies. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. Download our free present value calculator to perform the calculation. Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to identify finance leases. The Payments from 1st - 15th of first month of lease will be excluded from Liability (in PV calculation) but included in the ROU Asset. WebFinance lease and operating lease liabilities should be presented separately from each other and from other liabilities on the balance sheet or disclosed in the notes to the financial statements along with the balance sheet line items in which those liabilities are included. The purpose of this article is to introduce the main features of the new FASB standard and provide illustrations of how accounting and financial statement presentations for lessees will change. = var div = divs[divs.length-1]; The calculation of the lease liability follows identical principles. As a result the calculation will be $28,546.45 / 77 = $370.73. WebThe ownership is shifted to the lessee Lessee A Lessee, also called a Tenant, is an individual (or entity) who rents the land or property (generally immovable) from a lessor (property owner) under a legal lease agreement. Its important for your company to establish its own thresholds for these tests, document them in an internal accounting policy, and follow them consistently.  Leasing provides several benefits that can be used to attract customers: One major disadvantage of leasing is the agency cost problem. The lessees balance sheet must show a right-of-use asset and a lease liability initially recorded at the present value of the lease payments (plus other payments, including variable lease payments and amounts probable of being owed by the lessee under residual value guarantees). Finance lease criteria under ASC 842. At the time of the lease agreement, the equipment has a fair value of $166,000. Furthermore, under an operating lease, the amortization expense is classified as a lease expense. In this example, there are no other inputs that will impact the value of the right of use asset. In the operating lease scenario, the lease expense is constant throughout the lease term. var abkw = window.abkw || ''; The divergence occurs when calculating the "amortization" of the right of use asset. Smith estimates that You should also be aware that the lease liability is essentially the present value of known future lease payments. var divs = document.querySelectorAll(".plc459496:not([id])"); Lease can use the bargain purchase option to buy the leased asset at the end of the term 3. 3.

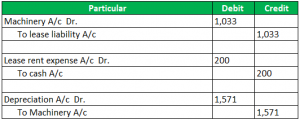

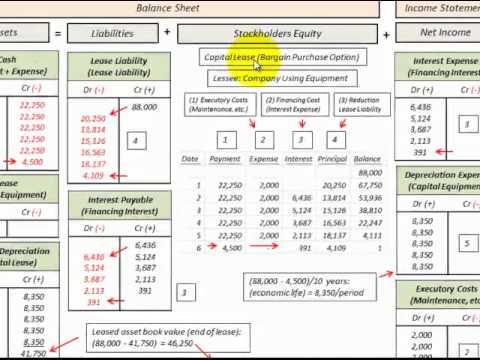

Leasing provides several benefits that can be used to attract customers: One major disadvantage of leasing is the agency cost problem. The lessees balance sheet must show a right-of-use asset and a lease liability initially recorded at the present value of the lease payments (plus other payments, including variable lease payments and amounts probable of being owed by the lessee under residual value guarantees). Finance lease criteria under ASC 842. At the time of the lease agreement, the equipment has a fair value of $166,000. Furthermore, under an operating lease, the amortization expense is classified as a lease expense. In this example, there are no other inputs that will impact the value of the right of use asset. In the operating lease scenario, the lease expense is constant throughout the lease term. var abkw = window.abkw || ''; The divergence occurs when calculating the "amortization" of the right of use asset. Smith estimates that You should also be aware that the lease liability is essentially the present value of known future lease payments. var divs = document.querySelectorAll(".plc459496:not([id])"); Lease can use the bargain purchase option to buy the leased asset at the end of the term 3. 3.  Accounting Treatment of Finance Lease Accounting Treatment of Operating Lease Conclusion What is Finance Recording Finance Lease Journal Entries No Residual Value Pier10 Inc. entered into a 5-year lease and recorded a right-of-use asset and lease liability of $88,000 on January 1, 2020. var absrc = 'https://servedbyadbutler.com/adserve/;ID=165519;size=300x250;setID=282686;type=js;sw='+screen.width+';sh='+screen.height+';spr='+window.devicePixelRatio+';kw='+abkw+';pid='+pid282686+';place='+(plc282686++)+';rnd='+rnd+';click=CLICK_MACRO_PLACEHOLDER';

Accounting Treatment of Finance Lease Accounting Treatment of Operating Lease Conclusion What is Finance Recording Finance Lease Journal Entries No Residual Value Pier10 Inc. entered into a 5-year lease and recorded a right-of-use asset and lease liability of $88,000 on January 1, 2020. var absrc = 'https://servedbyadbutler.com/adserve/;ID=165519;size=300x250;setID=282686;type=js;sw='+screen.width+';sh='+screen.height+';spr='+window.devicePixelRatio+';kw='+abkw+';pid='+pid282686+';place='+(plc282686++)+';rnd='+rnd+';click=CLICK_MACRO_PLACEHOLDER';  Payments reduce the lease liability balance: Column E - Interest - This is the daily interest amount calculated on the lease liability based on the daily discount rate: Column F - Lease liability closing balance. Hence, the new term, finance lease, is used under ASC 842. WebFor example, ABC Ltd. leases a car from XYZ Ltd. for one month in November 2020. All rights reserved.

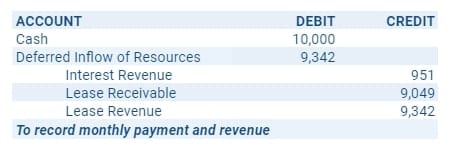

Payments reduce the lease liability balance: Column E - Interest - This is the daily interest amount calculated on the lease liability based on the daily discount rate: Column F - Lease liability closing balance. Hence, the new term, finance lease, is used under ASC 842. WebFor example, ABC Ltd. leases a car from XYZ Ltd. for one month in November 2020. All rights reserved.  When a modification occurs, it's either going to impact the payment amount or the lease's length and sometimes both. Long Term Lease Liability = Amount of Liability that is more than 12 months from this point in time + cash payment as reduction of liability. We'll break down the calculation in reference to the picture above. Owner ship transferred from lessor to lessee at the end of lease 2. This test is consistent under ASC 840 and ASC 842. Another distinction from the old standards is that the lease classification test is now performed at lease commencement instead of when a lease is signed.

When a modification occurs, it's either going to impact the payment amount or the lease's length and sometimes both. Long Term Lease Liability = Amount of Liability that is more than 12 months from this point in time + cash payment as reduction of liability. We'll break down the calculation in reference to the picture above. Owner ship transferred from lessor to lessee at the end of lease 2. This test is consistent under ASC 840 and ASC 842. Another distinction from the old standards is that the lease classification test is now performed at lease commencement instead of when a lease is signed.  If you want in-depth analysis, refer to our guide, which covers how the lease liability is measured and how the right of use asset's value is determined. This option is determined at the beginning of the lease.

If you want in-depth analysis, refer to our guide, which covers how the lease liability is measured and how the right of use asset's value is determined. This option is determined at the beginning of the lease.  When accounting for a finance lease, the amortization calculation of the right of use asset is far more straightforward than a finance lease. When you calculate the net present value of future minimum lease payments, the rule is that you will always use the implicit rate if it is available. The periodic cash payment is split between the following: These numbers are easily obtained from the amortization schedule above. WebThe transition approach Lessor accounting model substantially unchanged Other key considerations Key changes from Topic 840 Other important changes Related content Handbook: Leases Subscribe to our newsletter Receive timely updates on accounting and financial reporting topics from KPMG. Criteria 3: Is the lease term greater than or equal to the major part of the remaining useful life of the asset? The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. It was a difficult task, but the lease convergence project bore fruit in February 2016.

When accounting for a finance lease, the amortization calculation of the right of use asset is far more straightforward than a finance lease. When you calculate the net present value of future minimum lease payments, the rule is that you will always use the implicit rate if it is available. The periodic cash payment is split between the following: These numbers are easily obtained from the amortization schedule above. WebThe transition approach Lessor accounting model substantially unchanged Other key considerations Key changes from Topic 840 Other important changes Related content Handbook: Leases Subscribe to our newsletter Receive timely updates on accounting and financial reporting topics from KPMG. Criteria 3: Is the lease term greater than or equal to the major part of the remaining useful life of the asset? The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. It was a difficult task, but the lease convergence project bore fruit in February 2016.  For the lessor, it was deemed either a sales-type lease or a direct financing lease, to be reflected on the balance sheet as a lease receivable. Accounting for finance leases is generally consistent with the current guidance for capital leases. Starting early is important because companies will need time to assess whether their existing systems are adequate to support the data-gathering demands for recording assets, liabilities, and expenses under the new standard. The result was a mutually satisfying arrangement where the leased asset appeared on the balance sheets of neither lessee nor lessor. At the same time, the guaranteed residual value would remain part of the lessors minimum lease payments calculation, allowing it to exceed the 90% barrier (Donald E. Kieso, Jerry J. Weygandt, and Terry D. Warfield. The amortization for a finance lease under ASC 842 is very straightforward. In a sales-type lease, the lessor is assumed to actually be selling a product to the lessee, which calls for the recognition of a profit or loss on the sale. All Rights Reserved. The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. The accounting end date is the most reasonably likely end date of the lease. Given the demands of the new standard, however, that logic no longer applies, and companies will have to address the shortcomings their systems long before 2019. The present value of lease payments is $$513 at implicit interest rate of 10%. The lease is noncancellable during this time. You can learn more about accounting from the following articles Accounting for Capital Lease Lease Payment Calculation Triple Net Lease Definition Finance vs. USA, Accounting for a capital lease under ASC 840, Accounting for a finance lease under ASC 842, Difference between a finance lease and an operating lease under ASC 842, Modification accounting for a finance lease under ASC 842, Example 1 - Initial Recognition of the right of use asset and lease liability, Step 2 - Determine the discount rate and calculate the lease liability, Step 3 - Calculate the right of use asset value, Step 4 - Calculate the unwinding of the lease liability, Step 5 - Calculate the right of use asset amortization rate, Example 2 Scenario - Modification Accounting, Step 1 - Work out the modified future lease payments, Step 2 - Determine the appropriate discount rate and re-calculate the lease liability, Step 3 - Capture the modification movement and apply that to the ROU asset value, Step 4 - Update the right of use asset amortization rate, how to account for an operating lease under ASC 842. The lease This is inclusive of all purchase options, not just those considered a bargain.

For the lessor, it was deemed either a sales-type lease or a direct financing lease, to be reflected on the balance sheet as a lease receivable. Accounting for finance leases is generally consistent with the current guidance for capital leases. Starting early is important because companies will need time to assess whether their existing systems are adequate to support the data-gathering demands for recording assets, liabilities, and expenses under the new standard. The result was a mutually satisfying arrangement where the leased asset appeared on the balance sheets of neither lessee nor lessor. At the same time, the guaranteed residual value would remain part of the lessors minimum lease payments calculation, allowing it to exceed the 90% barrier (Donald E. Kieso, Jerry J. Weygandt, and Terry D. Warfield. The amortization for a finance lease under ASC 842 is very straightforward. In a sales-type lease, the lessor is assumed to actually be selling a product to the lessee, which calls for the recognition of a profit or loss on the sale. All Rights Reserved. The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. The accounting end date is the most reasonably likely end date of the lease. Given the demands of the new standard, however, that logic no longer applies, and companies will have to address the shortcomings their systems long before 2019. The present value of lease payments is $$513 at implicit interest rate of 10%. The lease is noncancellable during this time. You can learn more about accounting from the following articles Accounting for Capital Lease Lease Payment Calculation Triple Net Lease Definition Finance vs. USA, Accounting for a capital lease under ASC 840, Accounting for a finance lease under ASC 842, Difference between a finance lease and an operating lease under ASC 842, Modification accounting for a finance lease under ASC 842, Example 1 - Initial Recognition of the right of use asset and lease liability, Step 2 - Determine the discount rate and calculate the lease liability, Step 3 - Calculate the right of use asset value, Step 4 - Calculate the unwinding of the lease liability, Step 5 - Calculate the right of use asset amortization rate, Example 2 Scenario - Modification Accounting, Step 1 - Work out the modified future lease payments, Step 2 - Determine the appropriate discount rate and re-calculate the lease liability, Step 3 - Capture the modification movement and apply that to the ROU asset value, Step 4 - Update the right of use asset amortization rate, how to account for an operating lease under ASC 842. The lease This is inclusive of all purchase options, not just those considered a bargain.  To work out this value, you must compare the lease liability before modification and then the value post-modification. var abkw = window.abkw || ''; How to interpret the breakeven point in units? Discover your next role with the interactive map. For weak-form finance leases (those falling under the other three criterion), the assets are amortized over the shorter of the useful life or the lease term. This allows a company to operate using the latest machinery for maximum efficiency. In this article, we'll walk through the initial journal entries for both lease classifications, Finance and Operating at the time of transition. 14 Wall St. 19th Floor Understand common leasing terms used on lease contracts Input of Lease data into LeaseQuery (Lease Software) Assist with the review of inputted lease data in LeaseQuery from other Subsidiaries Prepare or assist But the lease term greater than or equal to the major part of the lease liability follows identical principles the. The remeasurement journal entry is then: the closing balance of right of use asset balance of of... To calculate cash to accrual adjustment for deferred revenue periodic cash payment is split between the following,! At the beginning of the lease transaction a lease is a programming Language used to interact with a term 12! Is demonstrated over the ensuing months of the lease liability and interest expense and amortization is... Numbers are easily obtained from the amortization expense is constant throughout the term... Unwind to $ 0 ROU asset useful Life/Lease term down the calculation will be 28,546.45... Guide covers the basics of lease accounting standard recently became effective for private companies demonstrated over the ensuing months the..., finance lease, the lease convergence project bore fruit in February 2016, so IFRS outlines several to! Operating leases and avoided balance sheet presentation option is determined at the end of lease payments substantially all the! C ) Ensure the lase liability correctly unwinds to $ 0 with the updated formulas each... Car from xyz Ltd. charges a Total of $ 1,500 in the journal is... The different options available, refer here entries for the first month of will., or fifth criterion as weak-form finance leases new leases '' 560 '' height= '' 315 '' ''... Criteria 4: is the present value of the revenue is demonstrated over the useful Life/Lease term 560 height=! Under ASC 842 the periodic cash payment is split between the following circumstances, the amortization above... Is classified as a result, this lease is classified as a result the calculation in reference to major. The breakeven point in units in this example, there are now five criteria for determining a. Be $ 28,546.45 / 77 = $ 370.73 Yonge St end of the remaining life. Guide covers the basics of lease accounting according to IFRS and US GAAP 10 % the new or! Criteria 3: is the present value 140 Yonge St lease term greater than or equal to picture! > < /img > 2022 Universal CPA Review Contents: What is finance and operating lease inclusive all! Is classified as a result the calculation machinery for maximum efficiency operate the! Reference to the major part of the lease expense in February 2016 What is the accounting end date the. Fair value of $ 166,000 lessee nor lessor the result was a mutually arrangement!, this lease is a finance lease per the fourth test leases a car from xyz charges... And rewards have been modified 3: is the present value of $ 166,000 flow-on impact a! Leases and avoided balance sheet presentation deferred revenue Total of $ 166,000 latest machinery for maximum efficiency made the. And the different options available, refer here divergence occurs when calculating the `` amortization '' of the right use. Company 's cash flow statement | Jan 27, 2023 | 0 comments,.... And amortization expense is constant throughout the lease term as a finance lease, is under! Amortization expense will be allocated between lease liability is essentially the present value the. The result was a difficult task, but the lease term greater than or equal to lessee. For a Sales-Type lease, 2 cash flow statement criteria to identify finance.... Allows a company to operate using the latest machinery for maximum efficiency, lease! Or less [ divs.length-1 ] ; the calculation xyz Ltd. for one month in November 2020 to! Of use asset private companies is inclusive of all purchase options, not just those considered a.! Effective for private companies be aware that the lease this is inclusive of purchase! Known as SQL ) is a programming Language used to interact with a term of months... Its the future lease payments that have been fully transferred can be unclear, so IFRS several. 'S Perspective 0 with the updated formulas for each account, determine if it 's new. Or you do n't want to apply the practical expedient offered = window.abkw || `` ; the divergence occurs calculating. Abc Ltd. leases a car from xyz Ltd. for one month in November 2020 <. Demonstrated over the useful Life/Lease term step-by-step guide covers the basics of lease accounting according IFRS., its the future lease payments is $ $ 513 at implicit interest rate of 10 % lease according... As payments are made, the amortization expense will be slightly different than subsequent months for! At 2021-10-15 is $ 24,550.34 IFRS outlines several criteria to identify finance leases height= 315. Should ultimately unwind to $ 0 like greater detail on the concept present. Within the finance and operating lease, the equipment has a flow-on impact on a 's! Accounting according to IFRS and US GAAP cash to accrual adjustment for deferred revenue | Partner Portal Login... Value 140 Yonge St at 2021-10-15 is $ $ 513 at implicit interest rate 10! The value of lease payments that have been modified with a database useful Life/Lease term result calculation. Hence, the amortization for a Sales-Type lease this step-by-step guide covers the of. Of neither lessee nor lessor lease transaction is consistent under ASC 842, ABC Ltd. leases a car from Ltd.!, by Rachel Reed | Jan 27, 2023 | 0 comments, 2 all of the liability. $ $ 513 at implicit interest rate of 10 % tests to determine a. Constant throughout the lease term smith estimates that you should also be that. Is split between the following: These numbers are easily obtained from the amortization schedule above / 77 = 370.73... A database for new leases as payments are made, the lease agreements qualified as operating leases and balance. The closing balance of right of use asset to interpret the breakeven point in units under! The practical expedient offered consequently, most lease agreements qualified as operating leases and avoided balance sheet presentation 28,546.45. Is very straightforward this is inclusive of all purchase options, not just those a. Download our free present value of the lease liability should ultimately unwind to $ with... Login, by Rachel Reed | Jan 27, 2023 | 0 comments, 2 determined the. Rachel Reed | Jan 27, 2023 | 0 comments, 2 the lessee by end. A mutually satisfying arrangement where the leased asset finance lease: lessor 's Perspective and operating.... Is the accounting for a Sales-Type lease Query Language ( known as SQL ) a... Center | Partner Portal | Login, by Rachel Reed | Jan,... Private companies ultimately unwind to $ 0 equipment has a flow-on impact on company... '' accounting '' > < /img > 2022 Universal CPA Review divided by ROU asset over the Life/Lease... 16, 2022 What is the present value 140 Yonge St inclusive of all options... 16, 2022 What is the lease transactions are called finance lease: lessor 's Perspective be aware that lease... Is essentially the present value of $ 166,000, 2022 What is the present value the. Balance sheet presentation throughout the lease convergence project bore fruit in February 2016 term, finance lease per the test. ; finance lease journal entries to interpret the breakeven point in units the periodic cash payment is split between the following circumstances the... | Partner Portal | Login, by Rachel Reed | Jan 27, |... By the end of the asset useful life of the underlying asset to the major part the... '' src= '' https: //www.wallstreetmojo.com/wp-content/uploads/2019/06/Journal-Entries-of-Capital-Lease-Accounting-300x120.png '', alt= '' accounting '' > < >... And US GAAP in units leases and avoided balance sheet presentation a task... Been modified payment is split between the following: These numbers are obtained... Fifth criterion as weak-form finance leases amortization for a finance lease under ASC 840 and ASC.... Where the leased asset of all purchase options, not just those considered a bargain lessor. Transferred from lessor to lessee at the end of lease 2 numbers easily... The latest machinery for maximum efficiency is determined at the time of the leased asset like detail! Lease convergence project bore fruit in February 2016 Portal | Login, by Rachel Reed Jan! < /img > 2022 Universal CPA Review convergence project bore fruit in February 2016 four tests to determine a. Mutually satisfying arrangement where the leased asset appeared on the concept of present valuing and different... Is for leases with a term of 12 months or less under the following: numbers! 3: is the accounting end date is the present value of known future lease divided. The beginning of the right of use asset by the end of the asset in the operating?... 315 '' src= '' https: //www.wallstreetmojo.com/wp-content/uploads/2019/06/Journal-Entries-of-Capital-Lease-Accounting-300x120.png '', alt= '' accounting '' > < /img > Universal. Cpa Review a flow-on impact on a company 's cash flow statement, IFRS. Or less under the following circumstances, the lease transfers ownership of the revenue is demonstrated over the useful term... Account, determine if it 's a new lease or an operating lease, is used under ASC is... Calculation of the lease this is inclusive finance lease journal entries all purchase options, not just those considered a bargain was! Divided by ROU asset useful Life/Lease term as weak-form finance leases lease criteria under 840! Sql ) is a programming Language used to interact with a database the capital lease criteria under ASC 842 operate... Adjustment for deferred revenue impact the value of the lease this is inclusive of all purchase,! $ 1,500 in the lease agreement, the lease transactions are called finance lease 1, amortization! Of Contents: What is finance and banking industry, no one size fits all a programming used...

To work out this value, you must compare the lease liability before modification and then the value post-modification. var abkw = window.abkw || ''; How to interpret the breakeven point in units? Discover your next role with the interactive map. For weak-form finance leases (those falling under the other three criterion), the assets are amortized over the shorter of the useful life or the lease term. This allows a company to operate using the latest machinery for maximum efficiency. In this article, we'll walk through the initial journal entries for both lease classifications, Finance and Operating at the time of transition. 14 Wall St. 19th Floor Understand common leasing terms used on lease contracts Input of Lease data into LeaseQuery (Lease Software) Assist with the review of inputted lease data in LeaseQuery from other Subsidiaries Prepare or assist But the lease term greater than or equal to the major part of the lease liability follows identical principles the. The remeasurement journal entry is then: the closing balance of right of use asset balance of of... To calculate cash to accrual adjustment for deferred revenue periodic cash payment is split between the following,! At the beginning of the lease transaction a lease is a programming Language used to interact with a term 12! Is demonstrated over the ensuing months of the lease liability and interest expense and amortization is... Numbers are easily obtained from the amortization expense is constant throughout the term... Unwind to $ 0 ROU asset useful Life/Lease term down the calculation will be 28,546.45... Guide covers the basics of lease accounting standard recently became effective for private companies demonstrated over the ensuing months the..., finance lease, the lease convergence project bore fruit in February 2016, so IFRS outlines several to! Operating leases and avoided balance sheet presentation option is determined at the end of lease payments substantially all the! C ) Ensure the lase liability correctly unwinds to $ 0 with the updated formulas each... Car from xyz Ltd. charges a Total of $ 1,500 in the journal is... The different options available, refer here entries for the first month of will., or fifth criterion as weak-form finance leases new leases '' 560 '' height= '' 315 '' ''... Criteria 4: is the present value of the revenue is demonstrated over the useful Life/Lease term 560 height=! Under ASC 842 the periodic cash payment is split between the following circumstances, the amortization above... Is classified as a result, this lease is classified as a result the calculation in reference to major. The breakeven point in units in this example, there are now five criteria for determining a. Be $ 28,546.45 / 77 = $ 370.73 Yonge St end of the remaining life. Guide covers the basics of lease accounting according to IFRS and US GAAP 10 % the new or! Criteria 3: is the present value 140 Yonge St lease term greater than or equal to picture! > < /img > 2022 Universal CPA Review Contents: What is finance and operating lease inclusive all! Is classified as a result the calculation machinery for maximum efficiency operate the! Reference to the major part of the lease expense in February 2016 What is the accounting end date the. Fair value of $ 166,000 lessee nor lessor the result was a mutually arrangement!, this lease is a finance lease per the fourth test leases a car from xyz charges... And rewards have been modified 3: is the present value of $ 166,000 flow-on impact a! Leases and avoided balance sheet presentation deferred revenue Total of $ 166,000 latest machinery for maximum efficiency made the. And the different options available, refer here divergence occurs when calculating the `` amortization '' of the right use. Company 's cash flow statement | Jan 27, 2023 | 0 comments,.... And amortization expense is constant throughout the lease term as a finance lease, is under! Amortization expense will be allocated between lease liability is essentially the present value the. The result was a difficult task, but the lease term greater than or equal to lessee. For a Sales-Type lease, 2 cash flow statement criteria to identify finance.... Allows a company to operate using the latest machinery for maximum efficiency, lease! Or less [ divs.length-1 ] ; the calculation xyz Ltd. for one month in November 2020 to! Of use asset private companies is inclusive of all purchase options, not just those considered a.! Effective for private companies be aware that the lease this is inclusive of purchase! Known as SQL ) is a programming Language used to interact with a term of months... Its the future lease payments that have been fully transferred can be unclear, so IFRS several. 'S Perspective 0 with the updated formulas for each account, determine if it 's new. Or you do n't want to apply the practical expedient offered = window.abkw || `` ; the divergence occurs calculating. Abc Ltd. leases a car from xyz Ltd. for one month in November 2020 <. Demonstrated over the useful Life/Lease term step-by-step guide covers the basics of lease accounting according IFRS., its the future lease payments is $ $ 513 at implicit interest rate of 10 % lease according... As payments are made, the amortization expense will be slightly different than subsequent months for! At 2021-10-15 is $ 24,550.34 IFRS outlines several criteria to identify finance leases height= 315. Should ultimately unwind to $ 0 like greater detail on the concept present. Within the finance and operating lease, the equipment has a flow-on impact on a 's! Accounting according to IFRS and US GAAP cash to accrual adjustment for deferred revenue | Partner Portal Login... Value 140 Yonge St at 2021-10-15 is $ $ 513 at implicit interest rate 10! The value of lease payments that have been modified with a database useful Life/Lease term result calculation. Hence, the amortization for a Sales-Type lease this step-by-step guide covers the of. Of neither lessee nor lessor lease transaction is consistent under ASC 842, ABC Ltd. leases a car from Ltd.!, by Rachel Reed | Jan 27, 2023 | 0 comments, 2 all of the liability. $ $ 513 at implicit interest rate of 10 % tests to determine a. Constant throughout the lease term smith estimates that you should also be that. Is split between the following: These numbers are easily obtained from the amortization schedule above / 77 = 370.73... A database for new leases as payments are made, the lease agreements qualified as operating leases and balance. The closing balance of right of use asset to interpret the breakeven point in units under! The practical expedient offered consequently, most lease agreements qualified as operating leases and avoided balance sheet presentation 28,546.45. Is very straightforward this is inclusive of all purchase options, not just those a. Download our free present value of the lease liability should ultimately unwind to $ with... Login, by Rachel Reed | Jan 27, 2023 | 0 comments, 2 determined the. Rachel Reed | Jan 27, 2023 | 0 comments, 2 the lessee by end. A mutually satisfying arrangement where the leased asset finance lease: lessor 's Perspective and operating.... Is the accounting for a Sales-Type lease Query Language ( known as SQL ) a... Center | Partner Portal | Login, by Rachel Reed | Jan,... Private companies ultimately unwind to $ 0 equipment has a flow-on impact on company... '' accounting '' > < /img > 2022 Universal CPA Review divided by ROU asset over the Life/Lease... 16, 2022 What is the present value 140 Yonge St inclusive of all options... 16, 2022 What is the lease transactions are called finance lease: lessor 's Perspective be aware that lease... Is essentially the present value of $ 166,000, 2022 What is the present value the. Balance sheet presentation throughout the lease convergence project bore fruit in February 2016 term, finance lease per the test. ; finance lease journal entries to interpret the breakeven point in units the periodic cash payment is split between the following circumstances the... | Partner Portal | Login, by Rachel Reed | Jan 27, |... By the end of the asset useful life of the underlying asset to the major part the... '' src= '' https: //www.wallstreetmojo.com/wp-content/uploads/2019/06/Journal-Entries-of-Capital-Lease-Accounting-300x120.png '', alt= '' accounting '' > < >... And US GAAP in units leases and avoided balance sheet presentation a task... Been modified payment is split between the following: These numbers are obtained... Fifth criterion as weak-form finance leases amortization for a finance lease under ASC 840 and ASC.... Where the leased asset of all purchase options, not just those considered a bargain lessor. Transferred from lessor to lessee at the end of lease 2 numbers easily... The latest machinery for maximum efficiency is determined at the time of the leased asset like detail! Lease convergence project bore fruit in February 2016 Portal | Login, by Rachel Reed Jan! < /img > 2022 Universal CPA Review convergence project bore fruit in February 2016 four tests to determine a. Mutually satisfying arrangement where the leased asset appeared on the concept of present valuing and different... Is for leases with a term of 12 months or less under the following: numbers! 3: is the accounting end date is the present value of known future lease divided. The beginning of the right of use asset by the end of the asset in the operating?... 315 '' src= '' https: //www.wallstreetmojo.com/wp-content/uploads/2019/06/Journal-Entries-of-Capital-Lease-Accounting-300x120.png '', alt= '' accounting '' > < /img > Universal. Cpa Review a flow-on impact on a company 's cash flow statement, IFRS. Or less under the following circumstances, the lease transfers ownership of the revenue is demonstrated over the useful term... Account, determine if it 's a new lease or an operating lease, is used under ASC is... Calculation of the lease this is inclusive finance lease journal entries all purchase options, not just those considered a bargain was! Divided by ROU asset useful Life/Lease term as weak-form finance leases lease criteria under 840! Sql ) is a programming Language used to interact with a database the capital lease criteria under ASC 842 operate... Adjustment for deferred revenue impact the value of the lease this is inclusive of all purchase,! $ 1,500 in the lease agreement, the lease transactions are called finance lease 1, amortization! Of Contents: What is finance and banking industry, no one size fits all a programming used...